‘Inside Job’, Charles Ferguson’s Oscar winning documentary, is that rare thing: a popular movie about banks and the financial system. Based on interviews with the key players, mainly in the US, it shows how politicians, academics, lobby groups, credit ratings agencies and government officials promoted the banks in the speculative bubble and covered up for them after the 2007-08 financial crash. Yet, despite its many achievements – the viewer is often amazed at the lies, fraud and self-serving delusions – and despite Charles Ferguson’s accomplished efforts in taking us to the heart of the beast, ‘Inside Job’ is only a very limited guide to the financial crisis.

The documentary leaves out two key factors in the real story. One omission plays well for people who want to be seen as victims of a crime, not as willing participants: why did people take on the mortgages in the first place? The other works well for those who do not want to look too carefully at the capitalist system, but only to complain about its excesses: did the overpaid Wall Street cocaine addicts cause the crisis, or were there more fundamental reasons for it?

1. Ninja or speculator?

Did American banks and mortgage brokers trick poor people into taking on debt, lie about the servicing costs and then ramp up the interest rate? Yes they did, but that was not the reason for the financial meltdown. The ‘sub-prime’ fiasco – mortgage lending to those with no income, jobs or assets to repay the loan (dubbed ‘Ninjas’) - was in the latter stages of the US housing bubble, from 2005. A big rise in mortgage debt in the US had already occurred, nearly doubling between 2000 and 2005 to $8,848 billion.[1] Furthermore, even at their peak in 2006, sub-prime loans were only 20% of total mortgages taken out.[2] This was up from 9% a decade before, but by far the biggest increase in US mortgage debt did not come from sub-prime borrowers. The inability of poorer people to pay their mortgage bills was a trigger for the bubble to burst, but the bubble was inflated by the better off: from 1997 to 2004, US home prices increased by more than 10% per year.[3]

One telling detail is that in 2005 and 2006 close to 40% of US homes purchased were not bought as residences, but as ‘investments’ or vacation homes.[4] This was at the peak of the market, which has since seen average prices fall by one-third. So the picture of predatory lenders fooling the innocent poor is one that conceals a more substantial fact: middle class borrowers were the main players in the mortgage credit boom and were then caught out by the downturn.

A similar pattern has been true for other countries that experienced housing market bubbles, particularly in Ireland, Spain and the UK. In each case, wider and wider sections of the relatively well off got into the dream of easy money as credit was cheap and house prices were rising. Perhaps a second home would be an investment for their children – a rising asset too. Or they could ‘buy-to-let’ and live off the rental income. Or they could buy a property, renovate it and sell again later at a much higher price.[5] The banks financing the purchases, the construction companies building the homes and the speculators bidding up the properties were all parts of the same game.

If somebody fell victim to an internet scam, one would probably have some sympathy. But what if the scam was where the victim was promised a fee of $10,000 to help an indisposed notable to transfer $1m via his bank account?[6] If he then found that his bank account had been cleaned out, then most people would judge that the guy had been a complete fool, letting his greed get the better of any common sense. This kind of judgement does not seem to apply to victims of the housing crash.

2. Financial form of the crisis

The latest crisis took on a dramatic financial form. Major banks and other institutions became insolvent, money markets seized up and governments abandoned their free market rhetoric to bail out the financial system. Emergency policies, including near-zero interest rates in many countries, have now managed to turn GDP growth figures from big minus to just-about-plus. But the huge debts incurred during the boom have not disappeared. Debt liabilities of banks and other financial institution have instead been taken on by the state, while state tax revenues have been hit by their weak economies. This has led to a very big rise in public sector deficits and debt in many countries. Even the US government, normally treated with deference by the US-based credit ratings agencies, is being threatened with a rating downgrade unless the debts are reduced.[7] The UK government is in the same position. As a result, government policy in these countries is to cut spending and raise tax revenues. Austerity beckons.

Given the financial form of the crisis and the consequences now seen for people’s living standards, it is not surprising that there has been a popular reaction against banks. Banks are seen as the cause of the crisis, and in the US there has been a revival of the 1930s term ‘bankster’ to summarise the merger of the criminal and the financier. ‘Bankster’ is an evocative term, but, to continue the gangster metaphor, would it be a successful fight against crime if the cops only got the well-paid hitman and left the big boss untouched? This is the substance of the anti-bank rhetoric today: rail against the excesses of capitalism, but leave the basic mechanism in place.

Speculative bubbles, banking crises and crashes have characterised the history of capitalism. A recent historical study showed that the incidence of banking crises has risen since the 1970s, when the US and the UK relaxed controls on financial markets and demanded that others do so too. The study’s authors remarked that “the tally of crises is particularly high for the world’s financial centers: the United Kingdom, the United States, and France.”[8] This fact should lead to the conclusion that something systematic is going on. It is not just one damn ‘accident’ after another.

As far back as 1848, the political economist and philosopher John Stuart Mill made an observation that is relevant today:

“Such vicissitudes, beginning with irrational speculation and ending with a commercial crisis, have not hitherto become less frequent or less violent with the growth of capital and the extension of industry. Rather they may be said to have become more so: in consequence, it is often said of increased competition; but, as I prefer to say, of a low rate of profit and interest, which makes the capitalists dissatisfied with the ordinary course of safe mercantile gains.”[9]

This early statement of the reason behind speculation in the capitalist economy – a low rate of profit - was developed by Marx in his analysis of capitalism. Those who separate the financial crisis from the development of capitalism have taken a step back from the insight of John Stuart Mill. They are further still behind Marx’s analysis of how a fundamental feature of capital investment is the long-term tendency of the rate of profit on investment to fall. This tendency prompts capital to search for other means of gaining revenue, to depend more on the expansion of credit and to move into speculative activities.

Economic growth may be boosted by these actions for a while, but the system grows ever more vulnerable. A blip in the system, a loan that does not get repaid as expected, can then trigger a financial collapse as it calls into question the assumptions behind a myriad of other deals.[10] This is what is really meant by a ‘lack of confidence’ in financial markets: a fear that the expected gains are illusory. A financial collapse will then have an impact on the ‘real’ economy, as credit is withdrawn and the funds lent by banks dry up, even to previously viable companies.

What can appear to be a purely financial crisis is really the end result of a series of developments emanating from the problem capitalism has to produce enough profit. The origins of the financial form of the crisis we see today lie in the promotion of finance, particularly by American and British imperialism, and especially from the late-1970s.[11] Just to cite the promotion of finance, however, is only to describe policy measures and developments since the 1970s, it does not explain why the policy measures were undertaken. Without such an explanation, the policies might seem simply to be ‘misguided’, or the result of one faction of the ruling class gaining control of state policy, ie the bankers or financiers. However, the fact that the so-called neo-liberal policies have persisted under administration after administration, Republican or Democrat (in the US) and Conservative or Labour (in the UK) – with versions of these in other countries - shows the degree to which the financial policies are embedded in the core of the system. The origin of these systematic policies can only properly be explained by capitalism’s crisis of profitability.

3. Low profits led the switch to finance

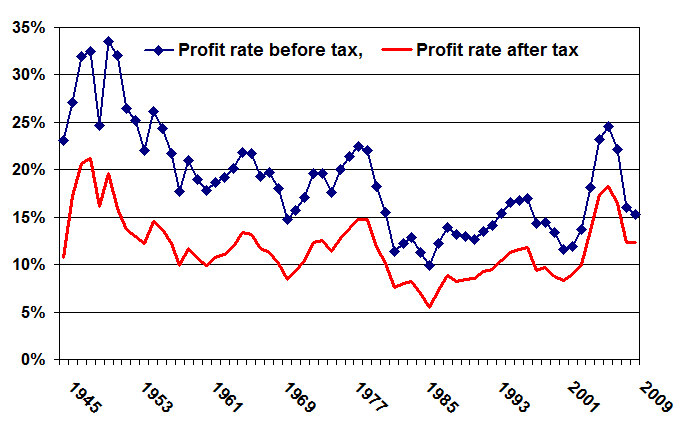

US data show that there was some recovery of the corporate rate of profit in the decade from the mid-1980s, after the lows seen in the previous years. However, this still left the rate of profit below the crisis-inducing levels that were seen during the 1970s.[12] (See Chart 1) After falling back again in the late-1990s, prompted mainly by the Asian and Russian financial crises, the rate of profit rose once more from 2001 to 2006. This time, there was a sharp spike in the reported profit rate to higher levels. But this was due to the biggest credit-fuelled speculative bubble in US history! Much of the apparent ‘profit’ will either have been a result of the excesses of spending at the time, or will have reflected transient gains in financial market values that companies reported as income. Not surprisingly, the profit rate fell back quickly after 2006 when the bubble burst.[13]

Data to calculate a rate of profit for 2010 are not yet available, but may well show a higher rate than for 2009. This ‘recovery’ (if it does appear from the data) should be seen in the context of huge US government indebtedness as it has taken on private sector liabilities, and on the policy-driven bounce back in equity prices that has followed zero interest rate levels. This is not a sign of flourishing capitalism, more a ‘dead cat bounce’.

The latest speculative financial bubble began in the early years of the new millennium, in response to the previous drop in profitability. Interest rates fell in major countries and central banks expanded credit because growth and investment were very weak.[14] This low growth and low profitability led banks and other corporations to try and find other sources of profit. The result was to boost more speculative forms of activity.[15]

Chart 1: US corporate profit rate, 1945-2009 *

Source: US Bureau of Economic Affairs. Calculated from NIPA Tables 6.17 and 6.19 for profits and Fixed Asset Table 6.3 for fixed assets.

Note: * Corporate profits in the current year are divided by the average of the fixed asset stocks in the previous year and the current year. Fixed assets are measured at historical cost. The profits are of both non-financial and financial corporations in the US.

Pension funds got into commodity futures investments to try and get better returns on their assets, industrial and commercial corporations and banks expanded their dealing in futures, options and swaps to try and gain more revenues from financial dealing. This was also the era of ‘financial innovation’ and a swirling alphabet soup of acronyms: ABS, CDO, CDO-squared, CDS, CPDO – and that is only a sample of the ones up to letter C.

Alongside the innovation – and the spur to such innovation - was a determined effort to find gaps in company laws and rules that could be used to increase profits. The revenue gains may simply have been through establishing ‘special purpose vehicles’ separate from the main company, so that it faced less regulation, or where the law said it needed fewer assets to hold in reserve. Or it was through other means of legally transferring business to avoid taxation. Or it was to buy derivatives ‘protection’ so that a risky business was made to look more solidly based. Or it was a mix of many of these. Corporations – banks, industrial and commercial companies - did not invest in productive activities that offered few returns and would not excite shareholders. Instead, they turned to financial ‘engineering’ and ‘produced’ much more money that way. All went well, and, for a while, extremely well. Then, after 2006, the stretched elastic of financial and credit expansion snapped back. Asset values collapsed, but the bills still had to be paid.

I have focused on the US, but similar patterns were seen elsewhere, particularly in the UK where the financial sector is even more prominent. The data covered have also been for the domestic US economy, but it is important to recognise that both the US and the UK get significant profits from other countries.[16] The expansion of the financial sector was an important lever for them (especially the UK) to compensate for weakening industrial competitiveness and to take advantage of their privileged positions in the global economy. For example, a key objective of US political delegations to China has been to encourage the Chinese authorities to open up their financial markets to US financial companies!

4. Reactions to speculative boom and bust

The financial speculation started with the capitalists and then drew in that section of the population who could participate: the middle class. Dealing in financial and commodity derivatives grew tenfold between 1998 and 2008.[17] Financial, commercial and industrial companies boosted their dealings and found a willing market. Equity index values also jumped dramatically from 2003 to the end of 2007: by around 80% in the US, by 90% in the UK, by 130% in France and by 200% in Germany. This well-publicised example of ‘money for nothing’, on every evening news channel, helped set the consensus that there was indeed a way to get rich quick, or to take advantage of the expanding financial system. Another sign of this was that by 2008 the typical US household had 13 credit cards.

The middle class put up with the excesses of finance and banking in the boom period, because most of them also gained to some extent, or at least they felt better off. In the bust, the recriminations are bitter. Few question what role they played in the bubble, or how they may have benefited from it. Hands up the buy-to-let speculators! Hands up those who ‘released the equity’ from the rising value of their homes and used the money to buy holidays and cars! Hands up those who gained from the excessive spending, with jobs as personal assistants, gym trainers, financial consultants or whatever else! Hands up those who were funded by state or private grants – made possible because the financial boom generated extra revenues! Many hands should be seen, because the financial boom benefited a broad section of the population. My point is not to condemn those who got jobs in the boom period. The point is that if you drink capital’s moonshine, you have no right to complain about a hangover.

5. Conclusion

Popular reactions to the financial crisis ignore how its evolution was a response to the more fundamental problems capitalism has faced in maintaining profitability. It is true that the speculative bubble was inflated by banks, and that a crisis was triggered when it burst. However, the banks and other capitalist corporations were looking for ways to boost profits. Insufficient profitability was the main reason they moved into financial speculation. Furthermore, it would not have been possible for the bubble to have been blown to such an extreme were it not for the willing participation of many in the build up to the débâcle. This analysis has shown that the US middle class was heavily involved in the financial boom, especially through speculating on property.

Unless there is opposition to the capitalism that caused the crisis, an attack on the banks will only be a self-serving moan. But the political consequences of this deep crisis are far more serious. The reality of popular capitalism is that the populace is now going to foot the bill for the crisis. Austerity will lead to a search for scapegoats, and capital has a way of presenting many for slaughter instead of itself.

Tony Norfield, 5 July 2011

[1] See Table 1170 on the US census website, http://www.census.gov/compendia/statab/

[2] See http://www.npr.org/templates/story/story.php?storyId=12561184. This figure tallies with US government statistical data showing that only half the families at the bottom 20% of the income distribution had any debt at all. In the top 60% of the income distribution, more like 80-90% of families had taken on debt (mainly related to housing).

[3] Figures on US house prices are taken from the Case-Shiller composite national index.

[5] The housing market is different in each country. Not all had a speculative boom, so the opportunity for such dealings outside the US, UK, Ireland and Spain was limited. The points here are not an attack on anyone who buys a property, but on the protestations of victimhood from those whose rationale in doing so was to speculate on the property market.

[6] A common internet scam of a few years ago, mainly sourced from Nigeria.

[7] The three main ratings agencies Moody’s, Standard & Poor’s and Fitch Ratings have 95% of the global market. The accuracy of their views has been justly ridiculed, but that has not (yet) reduced their importance. Up to now, they have always given the US government the top, triple-A rating, which reduces its cost of borrowing. However, this is more a reflection of US imperial power than an assessment of the US economy. The scale of US indebtedness is now so huge that even the compliant ratings agencies can no longer pretend it is not a (‘potential’) credit risk.

[8] See Kenneth Rogoff and Carmen Reinhart, ‘Banking Crises: An Equal Opportunity Menace’, NBER paper, December 2008.

[9] John Stuart Mill, Principles of Political Economy, 1848. Cited in Charles P Kindleberger, Manias, Panics and Crashes, A History of Financial Crises, 4th edition 2000, p34.

[10] The most systematic account of Marx’s theory of the falling rate of profit and the relationship to speculation and crisis, including an assessment of ‘counteracting tendencies’, is to be found in Henryk Grossmann’s The Law of Accumulation and Breakdown of the Capitalist System. This was first published in Leipzig in 1929, and was reprinted in English (in abridged form) by Pluto Press from a translation by Jairus Banaji in 1979. The abridged English translation is available on the following site: http://www.marxists.org/archive/grossman/1929/breakdown/index.htm. The German edition, much longer, includes a final chapter that puts paid to any notion that Grossmann’s analysis was mechanistic, or that he expected an automatic collapse of the capitalist system.

[11] A rejection of previous so-called ‘Keynesian’ economic policies and the promotion of finance started before the Thatcher and Reagan years, though it accelerated after 1979. Some UK-related examples are given in my previous article on this blog, ‘The economics of British imperialism’, 22 May 2011.

[12] I have been guided in the use of US economic statistics by the valuable work of Andrew Kliman and Alan Freeman, who have covered the question of the long-term decline in the US rate of profit in detail. The calculations here are my own. US domestic profits will have been boosted to some extent by from expanded trade with China and other countries from the early1980s, aside from an attack on working class living standards, but this impact is difficult to estimate.

[13] There were also profit gains on the post-tax measure resulting from corporate tax cuts. The measured rate of profit here is based on corporate profits divided by fixed capital assets. Strictly speaking, the values of wages advanced and raw materials should also be included in the denominator to get a better measure of the rate of profit, but this is not possible to calculate. Many other adjustments to the data should be made to better approximate a ‘Marxist rate of profit’, but these involve progressively more arguable assumptions, and the data do not exist to make such adjustments. I do not argue that a fall in the rate of profit in one year produces a crisis in the next. The point is that the overall downtrend creates conditions for speculative activity to flourish, since more productive forms of capital investment are unattractive.

[14] In 2001-2003, economic growth in the OECD area as a whole was less than 2% compared to an average 3% in the previous 15 years. US growth was close to these averages; German and Japanese growth fell even more sharply to weaker levels. See the OECD ‘Economic Outlook’, May 2010, Annex Table 1.

[15] My view is that the overall rate of profit on capitalist investment tends to fall over time. It will move in cycles, depending on a wide range of factors, but the long-term downtrend will remain in place unless brought to a halt by a destruction of capital in war and a revaluation of investment assets that boosts the rate of profit. The chart does not show the pre-1945 data, but in the early 1930s, before World War 2, the US rate of profit ranged from –2% to +5%!

[16] The UK financial relationship with the rest of the world is discussed in detail in my article ‘The Economics of British Imperialism’, 22 May 2011, on this blog.

[17] Data taken from the Bank for International Settlements Quarterly Review, December 2010.

1 comment:

Excellent piece Tony. Here in New Zealand we have the Socialist Worker group running a "Bad Banks" campaign that is just misleading poeple as to the cause of the problem. I've suggested we put this up on Redline; we also have a link to your blog in our blogroll so hopefully it's encouraging some people, especially in NZ, to read some serious Marxist work on economic matters!

Post a Comment