The US government could shut down next week if Congress does not agree to raise borrowing limits. If the government shuts down, then the US could also default on its debts and add another dimension of crisis to the global economy. Here I argue why the US will not default, but also why this is not the real debt problem that the US faces.

Default or not

There are two reasons why the US will not default and, incidentally, why financial markets are not in a state of panic. Firstly, there has been a government shut down five times since 1981, as cash ran out and a new budget limit was not agreed on schedule. Hundreds of thousands of federal employees were told to go home, and many ‘non-essential’ services were stopped. However, on none of the previous occasions was there a risk that the US government would fail to pay its debts and default. Money to cover the debt and interest payments was always found from somewhere, and paid on schedule.

Secondly, it is the US Congress that will decide the new borrowing limit after wrangling over tax and spending plans. This is not a limit imposed by some external body, not by the IMF, nor by a foreign power. If Democrats and Republicans agree on a deal, then this particular crisis will be over.

The only caveat is that it is hard to over-estimate the recklessness of America’s radical right. They could block a deal in order to press their objective to slash welfare payments and stop taxes rising. However, if that meant the US failed to maintain its debt payments, their political victory would be crowned by financial chaos. Such an outcome is possible, but very unlikely because of the consequences of a default. It would be a trigger for America losing its triple-A credit rating, which would feed through to all US companies. As credit ratings fall, borrowing becomes more expensive and less easy for everybody, something that these representatives of the highly indebted US economy are unlikely to risk, whatever their supposed opposition to ‘big government’.

A mere $14.3 trillion?

The federal government borrowing limit is $14.3 trillion, and the current debate is about making it bigger.[1] This sum close to 100% of US GDP, up from 65% just four years ago, and the curve is on a steep ascent. But, although massive, it does not include other government liabilities taken on after the financial crisis struck. The biggest of these is the $5 trillion of potential payments from the nationalised housing agencies, Fannie Mae and Freddie Mac. Furthermore, the US excludes from its debt figures the huge and unfunded obligations to pay future social security and medical bills.

The size of the US government debt relative to the economy is not unusual for major capitalist countries today, as a glance at Europe will testify. However, that is not the only problem. Far bigger than the government debt is borrowing by America’s private sector. This is sometimes ignored, on the blinkered view that private sector liabilities will ‘sort themselves out’ and trouble will only emerge from public sector debts. But that not only leaves out of account the $2.4 trillion of consumer debt, household mortgage debt of $10.1 trillion and business debts of another $10.9 trillion.[2] It also ignores the more fundamental problem of the whole economy.

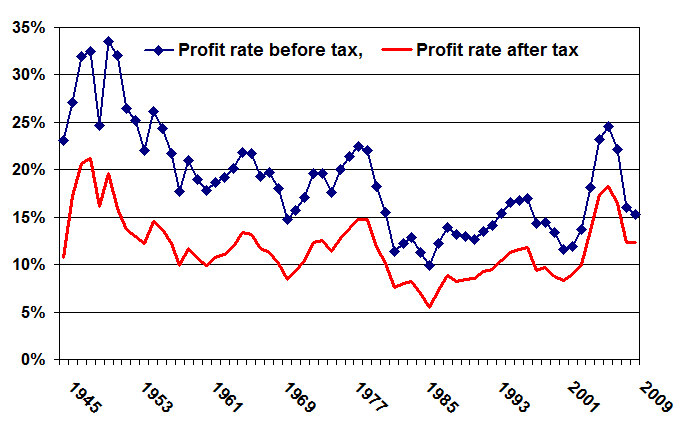

Borrowing, both by the private sector and the government, grew in response to the crisis of capital accumulation and low profitability. Credit growth then accelerated in the speculative bubble after 2001.[3] Now the bubble has burst, leaving the whole economy drowning in debt. The Federal Reserve has kept interest rates at close to zero, hoping to keep the debt servicing sustainable for a bit longer, and hoping that the economy will recover. But it doesn’t, and meanwhile the Fed itself is also the owner of a mountain of US debt. Its balance sheet has grown from less than $900bn at the start of 2008 to a giant $2.8 trillion by June this year, following its ‘quantitative easing’ programmes. Around $1.6 trillion of this is US Treasury debt and another $900bn or so is made up of mortgage-backed securities that banks cannot sell.

The squabble between Democrats and Republicans over the debt limit ceiling is really about the looming bankruptcy of the country. That is why each party has to claim that it plans to cut the level of debt over the next decade, despite finding themselves having no choice but to raise the ceiling still further.

The foreign dimension

There has been a steady build-up of US borrowing from other countries too. This is shown in the persistent annual current account deficits, where the US imports more goods and services than it exports. Details of the funding of these deficits end up in the figures for the US international investment position. These figures are the best summary of America’s accumulated assets and liabilities with the rest of the world. At the end of 2010, net US foreign liabilities amounted to $2.5 trillion.

In other words, the US owns far fewer assets (ownership of companies, bonds and equities) in other countries than foreigners own in the US. That is a weakness, but so far it has not shown up as a problem. The US still manages to earn more on its smaller assets than it pays on its bigger liabilities. For example, in 2010 the US earned net investment income of $171bn. This extraordinary feat of making a lot of money on a net debt position is rivalled only by the UK.[4]

America can do this because it takes full advantage of its imperial position in the global economy: the US dollar is the world’s major reserve currency, based upon the global dominance of the US economy, banking and finance. Despite America’s relative economic decline in recent decades, it remains the major imperialist power, with not only an extensive military but also a dollar-centred financial infrastructure. There has been little challenge to this position so far. The euro countries have their own problems, and China is still some way from building a financial platform in the world economy.

America’s ability to earn large investment revenues is based on two key factors. Firstly, it has a surplus of foreign direct investment assets, and its return on these investments is far more than it pays for foreign direct investment in the US. For example, in 2010 it earned $275bn more than it paid on this account. Secondly, its net liabilities are for securities that pay only a small return, especially on government bonds, but also on corporate bonds and equities. By the end of 2010, foreign central banks and private investment funds owned $5 trillion of US government securities that were earning minimal rates of interest. These low rates were acceptable to foreign investors because the US government debt market is one of the few that is big enough easily to take flows of global capital, it was denominated in the most important global currency, the dollar, and America’s triple-A credit rating also promised maximum security.

The Triple A question

The US is given a credit grade of AAA by the three major US-based agencies that account for 95% of the ratings market. However, even these have recently become concerned about the escalation of US debts. Formerly they were impressed by America’s imperial might and its ability to borrow in its own currency. Now the numbers have become embarrassing, and some agencies threaten to cut the rating if no credible plan to control future debt is made. They have also warned that if the US government missed any debt interest payments, even if only temporarily, this would be labelled a default and the US would be downgraded.[5]

The loss of its triple-A rating would not only be a humiliation for the world’s major imperialist power. It would cost money too. The cost of borrowing would rise not just for the government, but for all US companies. Even a rate rise of just 0.1% would result in many billions of dollars of extra interest payments when the scale of debt is so high.

A credit downgrade could also lead foreign investors to buy fewer US bonds. That will matter for a country whose current account deficit was $470bn last year. There is a further risk that investors sell some of their existing bonds. Even a very small percentage sale would be dramatic, since the stock of bonds held by foreign investors is so big: $8 trillion, including corporate bonds. This would bring a funding crisis and a slide in the US dollar on foreign exchange markets.

Up to now, global financial markets have used America and the dollar as the benchmark for security. Seeing this benchmark shaken will lead many more to think that global capitalism is not as solid as it pretends to be.

Conclusion

A US credit default is much more important than a Congressman might recognise. However, US capital is likely to make it clear to its political servants that risking a default is more than their jobs are worth. That is why we are much more likely to see a budget deal that agrees to domestic austerity at home, in some form or another, rather than one that risks further the vulnerable global status of US imperialism. Yet, even if a deal is done in the next week, one day the cheque will bounce.

Tony Norfield, 26 July 2011

[1] The $14.3 trillion is made up from $9.7 trillion in debt held by the ‘public’, ie outside the government in the form of US Treasuries, etc, and another $4.6 trillion held by other government bodies. This latter amount represents borrowing from the surpluses of the Social Security Trust Fund and other government funds to finance spending. It should definitely be included in the borrowing total.

[2] These debt figures are for the end of 2010. See the Federal Reserve report on this topic, Table D.3 in http://www.federalreserve.gov/releases/z1/Current/z1r-2.pdf

[3] See the article ‘Anti-Bank Populism in the Imperial Heartland’ on this blog, 5 July 2011, for details.

[4] See the article ‘Economics of British Imperialism’ on this blog, 22 May 2011.

[5] See Bloomberg News, ‘Moody’s Downgrade Warning Adds Pressure on US Debt Deal’, 14 July 2011.